One Problem, and a Three-Step Solution: How to Achieve Bank Primacy with Industry Intelligence as a Differentiator in the Middle Market

Guest authored by our friends at IBISWorld

Jim Fuhrman

Vice President of Client Services | Commercial Banking

IBISWorld

Posted: Jan 22nd, 2026

For the banking industry, 2026 is only beginning to unfold. Increased consolidation mixed with an appetite to rapidly scale technologies raises an uncomfortable but necessary question that frames the conversation: Are you the primary bank, or simply one of several providers? The difference is measurable, and the outcome may already indicate performance leading into 2027, as research shows primary banks influence decisions while secondary banks are left to compete on margins.

Particularly within the middle market ($10MM-<$500MM in annual sales), the average company uses roughly 11.8 financial products, and nearly 80% of those products sit with the primary bank. The goal, therefore, becomes the quest to maintain, or achieve in the first place, primacy, and the benchmark is clearly set at 4/5 of wallet share.

This distinction is becoming more important as banks rethink growth strategies. For years, commercial real estate (CRE) lending drove balance sheet expansion – offering hard collateral, familiar underwriting and efficiency. Commercial and industrial (C&I) lending, while strategically superior for deposits and long-term relationships, required deeper engagement, stronger operating insight and greater industry understanding. As a result, it often lagged CRE in priority.

That imbalance is now correcting. Regulatory scrutiny, concentration limits and uncertainty in CRE portfolios have pushed banks toward renewed optimism around C&I lending. Many institutions are entering 2026 with aggressive C&I growth targets, largely focused on expanding lending within their existing deposit base. The strategy is sound – but execution hinges on one critical factor: industry intelligence flowing consistently across the organization.

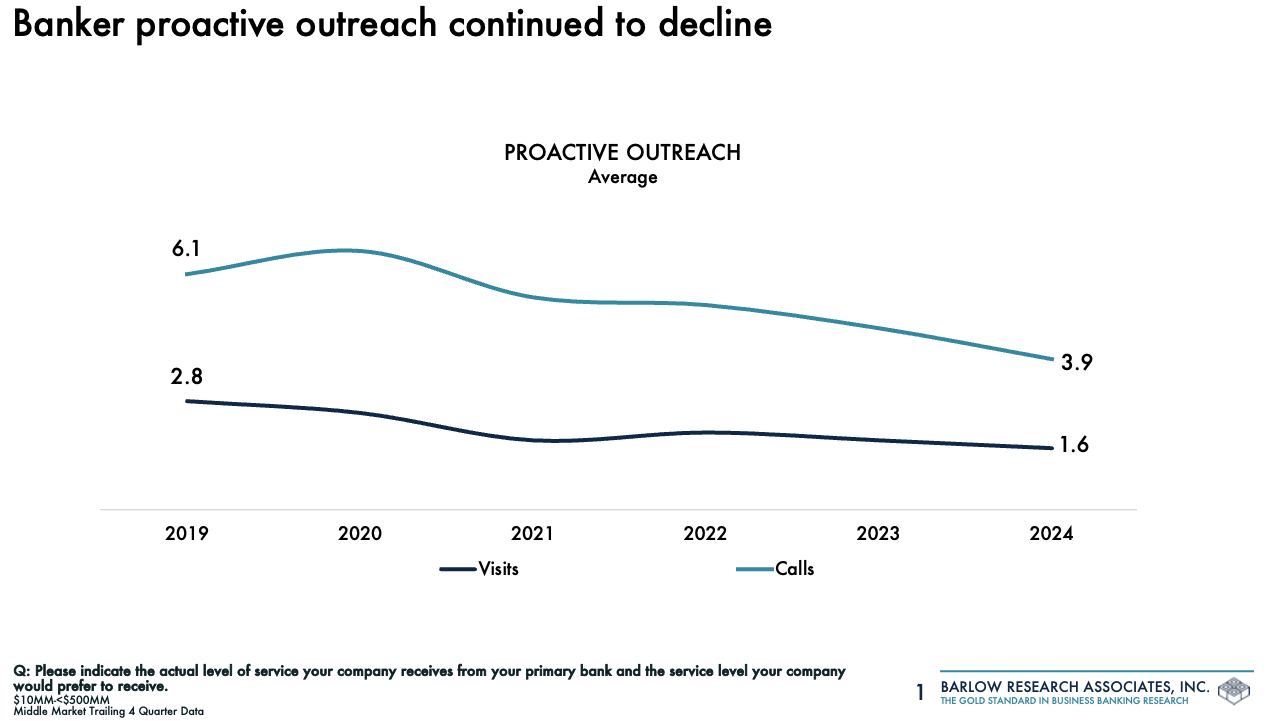

The challenge is engagement. Barlow Research’s latest data shows proactive outreach in the middle market has fallen to historic lows, with relationship managers (RMs) making 2.2 fewer phone calls and 1.2 fewer in-person visits per client annually than five years ago (see chart below). At the same time, responsiveness has slowed, weakening perceptions of value and trust. These declines correlate directly with poorer RM performance ratings – especially around understanding cash flow, company objectives, and proactively recommending solutions.

Industry specialization offers a proven way to reverse this trend, and three valuable touchpoints can make all the difference. Nearly 70% of middle market companies rate a banker’s industry knowledge as a top priority or very important, yet only about half of relationship managers are rated highly on sector expertise. The result is a persistent expectation gap – and a missed opportunity.

From there, industry insight becomes the backbone of RM engagement. Research-enabled conversations transform routine check-ins into meaningful advisory moments. A check-in becomes a discussion about sector benchmarks, shifts in working capital cycles or emerging risks – replacing the 2.2 “lost” calls with purposeful interactions that build trusted advisor status.

More importantly, industry fluency changes the nature of engagement itself. A “check-in” is no longer a calendar obligation; it becomes an opportunity to discuss sector-wide margin pressure, shifts in working capital cycles, labor constraints or demand forecasts. An RM might ask, “We’re seeing receivable days stretch across your industry – how is that affecting liquidity?” or “Peers are investing in automation to offset wage inflation – how are you thinking about capital deployment?” These questions demonstrate preparation and context, positioning the banker as an operational advisor rather than a product intermediary.

This shift is especially critical in the middle market, where many companies operate without boards of directors or formal centers of influence. In these environments, the banker often fills the advisory gap. While accountants and attorneys remain important partners, their involvement is episodic. Relationship managers who consistently bring industry insight into conversations earn the role of first call – well before a credit, treasury, or capital decision becomes urgent.

What leading banks increasingly recognize is that industry data cannot live in silos. It must move from marketing to relationship management to underwriting to portfolio oversight, using a shared, trusted source. When industry intelligence is consistent across the organization, engagement improves, decisions accelerate and risk is better managed.

This end-to-end alignment depends on reliable data. As banks invest in AI, automation and advanced analytics, the quality and consistency of industry information matter more than ever. Smarter tools require credible inputs. Without trustworthy data, speed becomes a liability rather than an advantage.

That reality is driving heavy investment in third-party integrations and APIs. Banks want industry insight delivered directly into CRMs, loan origination systems, underwriting platforms and portfolio dashboards – so better decisions can be made earlier. These integrations ensure that marketing, RMs, credit and risk teams are working from the same source of truth.

When industry data flows seamlessly across the organization, everyone truly “sings from the same songbook.” Messaging aligns with underwriting. Engagement aligns with risk appetite. Growth aligns with strategy. And most importantly, clients experience consistency – reinforcing trust.

As banks pursue ambitious C&I growth targets in 2026, success will not come from isolated initiatives. It will come from connecting industry intelligence across the enterprise, empowering bankers to engage with confidence and anchoring decisions in reliable data. In the middle market – where the primary bank captures both wallet share and influence – that alignment is foundational to durable growth.

How do you put this into action?

How Industry Knowledge Deepens a CRE Client into a C&I Relationship – and a Source of Referrals

As banks look to rebalance portfolios and expand C&I lending, many relationship managers assume resistance is the primary obstacle. In reality, the more common challenge is far simpler: the client does not realize their CRE bank can support the operating side of the business. Educating businesses of your financial solutions is key, and the opportunity to educate comes from building a brand as their trusted advisor. Trust begins by demonstrating your understanding of the dynamics that surround their business. This all-too-common case – where banks feel resistance is the obstacle – illustrates how to bridge the gap, and how industry fluency becomes the catalyst for deeper engagement.

Brief Case Study: A Narrow but Stable Relationship, Leaving Opportunity on the Table

The client was a middle market manufacturer with multiple properties financed through the bank. The relationship was profitable, long tenured and firmly anchored in commercial real estate lending. Outside of property loans and basic deposit accounts, however, the client used few additional banking services.

Importantly, this was not a case of dissatisfaction, but education. The business owner viewed the bank as reliable and responsive, but only in the context of real estate. He had never considered the bank a resource for working capital, equipment finance or broader C&I solutions – and therefore the manufacturer sourced financing elsewhere when it came to acquiring new machinery. Not because of a negative experience, but because no one had ever shown him otherwise.

Understanding the Owner’s Reality

The owner was deeply involved in day-to-day operations. He worked in the business, not on it. There was no board of directors, no internal strategy team and no formal financial advisor. Decisions were shaped by experience, habit and a small circle of external influences – primarily long-standing suppliers and service providers.

While those supplier relationships had existed for years, they were transactional by nature. Their bankers were largely absent from the conversation, providing little insight into cost dynamics or capital planning. As a result, the owner struggled to see how rising input prices – particularly raw materials and freight – were quietly compressing margins. The numbers were there, but the story behind them was not.

The Catalyst: Industry Knowledge, not a Product Pitch

The turning point came when the relationship manager reframed outreach around industry insight rather than financing. Instead of discussing loans or renewals, the RM initiated a short conversation about trends in paint manufacturing – specifically input cost volatility, labor constraints and the growing need for automation.

For the first time, the owner heard his own challenges described in industry terms. When the banker asked how resin pricing and transportation costs were impacting margins, the owner paused. He admitted that while costs had risen, he hadn’t fully connected those increases to cash flow strain. He was too close to daily operations to step back and analyze the impact holistically.

That moment changed the tone of the relationship. The banker was no longer just the “real estate lender,” but someone helping the owner understand his business in a broader context.

Education Creates Engagement

A follow-up conversation went deeper. Using industry benchmarks as reference points, the RM helped the owner think through how peers were responding – adjusting working capital structures, financing equipment to preserve liquidity and tightening cash conversion cycles through treasury tools.

Crucially, this was when the owner realized something he had never considered: his bank could support these needs. He had assumed operating credit, equipment financing and treasury solutions belonged elsewhere, often through supplier-affiliated lenders or institutions that had little understanding of his business.

With no board of directors and limited external guidance, the owner relied heavily on this new source of education. The banker’s ability to translate industry trends into practical financial options created trust and curiosity.

The Expansion and the Unexpected Outcome

An in-person meeting followed, focused not on selling products but on aligning the business’s capital structure with how it actually operated. The result was a modest C&I facility, equipment financing to support operational efficiency and treasury services to improve cash flow visibility.

But the impact extended beyond the balance sheet. As the owner began discussing these conversations with peers and suppliers, it became clear that many faced similar challenges and similarly lacked informed banking support. Several of those businesses were eventually introduced to the same banker, creating new referral opportunities rooted in credibility rather than solicitation.

Lessons for Bankers

This case highlights a critical reality for banks transitioning from CRE to C&I growth: many clients are not opposed to expanding the relationship – they are simply unaware it is possible. In the middle market, where owners often lack boards and operate deep inside their businesses, education is the gateway to engagement.

Industry knowledge changes the conversation. It helps owners see their businesses differently, recognize emerging pressures and understand their options. When that knowledge comes from a trusted CRE banker, it not only expands the relationship, it positions the banker as a valued center of influence, capable of generating growth well beyond a single client.

For banks seeking C&I momentum in 2026, the opportunity may already be on the books. The catalyst is not a new product, but a better conversation.

A Three-Step, Evidence-Based Path to Bank Primacy

Achieving bank primacy in the middle market is measurable and repeatable. Research and real-world experience point to three clear steps banks can take to strengthen engagement, expand C&I relationships and capture greater wallet share.

Step One: Equip Relationship Managers with Industry Fluency

Middle market clients are clear about what they value. Nearly 70 percent rate a banker’s industry knowledge as a top priority or very important, yet only about half of relationship managers (RMs) are rated highly on sector expertise. This disconnect directly impacts trust and performance.

Barlow Research’s data shows that RMs who lack an understanding of client cash flow and business objectives receive lower performance ratings. Once RMs demonstrate an understanding of industry dynamics, the conversation opens avenues of growth for the overall relationship.

Industry fluency is the starting point for relevance. Without it, relationships remain narrow and transactional, leaving profits on the table.

Step Two: Anchor Client Conversations in Industry Insight

RM engagement in the middle market has declined, with bankers making 2.2 fewer phone calls and 1.2 fewer in-person visits per client each year compared to five years ago. At the same time, slower responsiveness has weakened perceptions of value.

Industry insight helps reverse this trend by improving the quality of interactions. Conversations grounded in sector benchmarks, working capital trends and emerging risks replace generic check-ins with advisory dialogue. Questions about receivable cycles, margin pressure or automation trends signal preparation and context.

In the case study, a strategic pivot to introduce cash flow to the conversation could have opened the borrower’s eyes to the bank’s capabilities. However, the relationship, albeit stable, remained shallow.

Step Three: Embed Industry Intelligence Across the Enterprise

Industry insight cannot scale if it lives in silos. Leading banks are aligning marketing, relationship management, underwriting and portfolio oversight around a shared, trusted source of industry data.

This alignment is increasingly critical as banks invest in AI, automation and analytics. Faster tools require better inputs. Without consistent industry intelligence, speed increases risk rather than reducing it.

As a result, banks are investing in integrations that deliver industry data directly into CRMs, loan origination systems and portfolio dashboards. When teams operate from the same context, decisions align with strategy, engagement aligns with risk appetite and clients experience consistency.

The Takeaway

Banks that achieve primacy follow a simple pattern. They build industry fluency at the RM level, use that insight to elevate client conversations and embed industry intelligence across the organization.

In the middle market, where the primary bank captures nearly 80 percent of wallet share, this approach is foundational. For banks pursuing C&I growth in 2026, the opportunity is not a new product. It is a better-informed, more connected way of engaging clients.

About the Author:

Jim is a seasoned Client Service professional with over a decade of experience helping banking institutions apply data-driven strategies to real-world challenges. At IBISWorld, he works closely with commercial banks to navigate economic shifts, regulatory change, and evolving customer expectations. His industry perspective emphasizes the role of macroeconomic trends, digital transformation, and personalized banking in shaping competitive strategy, and he is a frequent speaker and contributor on how banks can translate market intelligence into execution.

Learn about our value to banks:

https://www.ibisworld.com/solutions/commercial-banking/

Vibe code our API solutions:

https://api.ibisworld.com/docs/-getting-started-1665865m0

For questions or feedback, contact: Jim.Fuhrman@ibisworld.com

About IBISWorld: IBISWorld delivers trusted, human-verified industry intelligence that helps commercial banking professionals make smarter, data-driven decisions throughout the credit cycle. Our Commercial Banking research equips banks with detailed performance data, financial benchmarks, risk indicators, economic trend analysis, and tailored insights to assess credit risk, uncover growth opportunities, strengthen underwriting and portfolio strategies, and support relationship-building with clients. Used by leading commercial banks worldwide, our solutions streamline lending, underwriting, and credit risk workflows with actionable benchmarks, industry ratios, and risk ratings that reveal both opportunity and potential threats across sectors. IBISWorld combines rigorously structured and contextualized data with advanced analytics – including AI-enabled tools that elevate insights without sacrificing accuracy – because reliable data is the foundation of effective intelligence and confident strategic decisions.