Business Optimism Fades as Costs and Geopolitical Risks Mount

Joel Mueller

Posted: May 14th, 2026

Businesses entered the second quarter of 2026 balancing cautious resilience with growing uncertainty. According to Barlow Research’s 2Q2026 Economic Pulse Study, both small businesses ($100K-<$10MM in annual sales) and middle market companies ($10MM-<$500MM in annual sales) remain concerned about elevated operating costs, fuel prices and geopolitical instability, particularly surrounding the Iran conflict and its impact on global energy markets. Yet most companies still expect to meet or exceed their financial goals in 2026 and continue to prioritize stability, liquidity and disciplined investment decisions.

Small business outlook

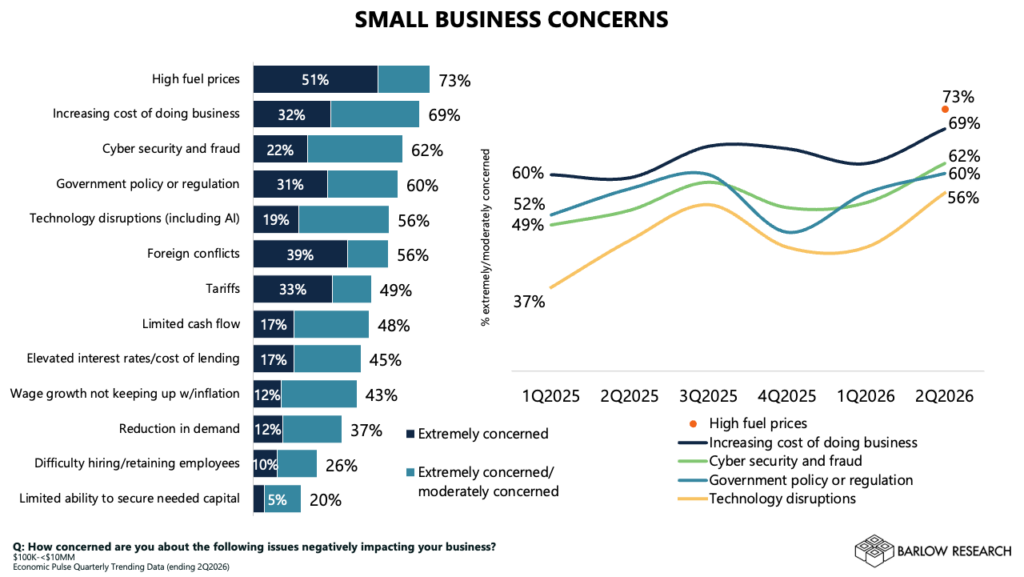

For small businesses, the environment remains challenging. Net difference overall financial conditions (the percent of businesses with deteriorated financial conditions subtracted from the percent of businesses with improved financial conditions) stayed slightly negative during the past 12 months. Although sales and profit trends improved modestly from the prior quarter, more businesses still reported declining sales and profits than increases. As shown in the graph below, 73% of small businesses report being concerned about high fuel prices negatively impacting their business, reflecting anxiety over international tensions and energy market disruptions.

Even with these pressures, small businesses showed signs of selective reinvestment. Capital expenditures rebounded sharply after reaching a low point in the first quarter, suggesting some companies are cautiously resuming investments in equipment and operations. Excess cash reserves also improved modestly, although liquidity concerns remain elevated for many firms. Looking ahead, small businesses appear increasingly focused on financial preservation rather than expansion. Profit expectations improved slightly, but sales expectations softened and hiring plans slowed. Businesses are placing greater emphasis on building cash reserves and managing costs as uncertainty around inflation, tariffs and fuel prices persists.

Demand for additional credit among small businesses remains subdued. Only 13% applied for additional credit over the past 12 months, and more than eight in ten either had no need for credit or chose not to borrow. Businesses that do anticipate borrowing are primarily focused on working capital needs rather than growth initiatives. Credit cards also became a more common financing tool, highlighting how smaller companies continue to seek flexible liquidity solutions while avoiding larger debt commitments in a high-rate environment.

Middle market outlook

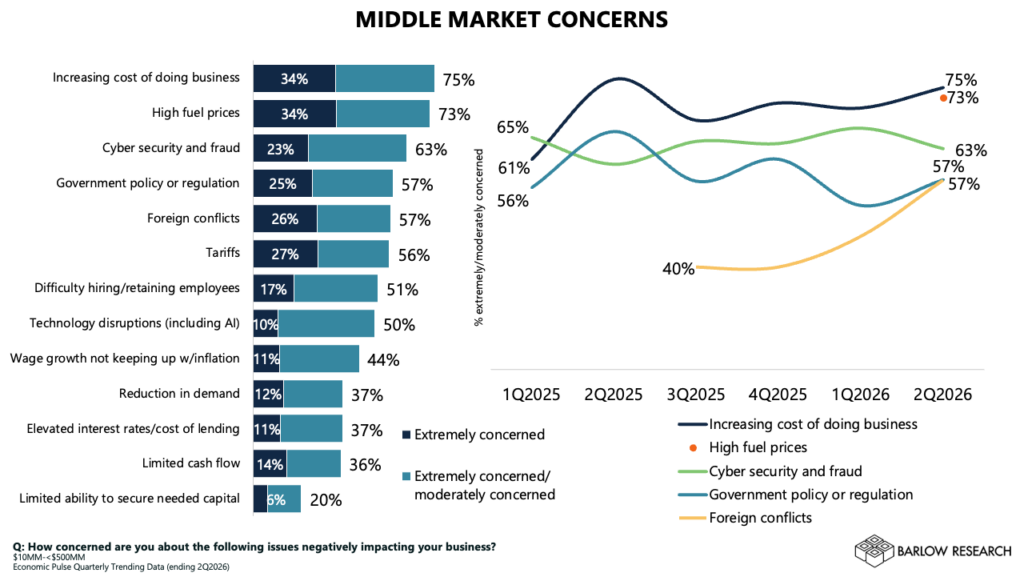

Middle market companies entered the second quarter from a somewhat stronger position. Overall financial conditions remained positive, and sales and profits improved during the past 12 months. Notably, net difference profits returned to positive territory for the first time in more than two years, signaling some stabilization after an extended period of margin compression. However, elevated operating costs continue to weigh heavily on businesses. Three in four middle market companies expressed concern about the increasing cost of doing business, while fuel prices and foreign conflicts also emerged as major worries (see graph below).

Middle market firms are becoming more cautious about the year ahead. While most still expect to meet or exceed financial goals, financial condition optimism weakened in the second quarter as fewer expect their overall condition to improve. Expectations for sales growth, profits, hiring and capital expenditures all declined from the previous quarter, with sales and profit expectations falling to their lowest levels in roughly two years. Companies appear to be shifting from aggressive growth strategies toward more measured and disciplined expansion plans as they navigate persistent uncertainty tied to tariffs, interest rates and geopolitical instability.

Middle market borrowing activity also softened after a period of stronger demand for additional credit. Fewer companies applied for additional credit in the second quarter, and expectations to borrow declined modestly as well. However, middle market firms remain substantially more active borrowers than small businesses, with commercial banks continuing to serve as the dominant financing source. Among companies expecting to borrow, most anticipate seeking loans of $1 million or more, primarily for equipment purchases, working capital and growth initiatives.

Key takeaways

For business bankers, the findings point to an environment where clients increasingly value strategic guidance, liquidity management and flexibility over aggressive expansion financing. Small businesses remain cautious borrowers focused on cash preservation and operational stability, while middle market companies continue investing selectively but are dialing back growth expectations. Conversations around working capital management, treasury solutions, rate sensitivity, fuel cost exposure and disciplined capital planning will likely become increasingly important as businesses navigate a slower and more uncertain economic landscape through the remainder of 2026.

- Small businesses remain financially cautious as elevated costs, fuel prices and softer sales expectations continue to pressure profitability, though selective reinvestment activity has started to return.

- Middle market companies remain in a stronger financial position overall, but weakening growth expectations and ongoing uncertainty around tariffs, interest rates and geopolitical tensions are driving a more measured outlook.

- Across both segments, businesses are prioritizing liquidity, cost management and operational stability, creating opportunities for bankers to provide strategic guidance and flexible financing solutions.

For more information about this article, the Economic Pulse Study or the Business Sentiment Tracking Study, email Joel Mueller at jmueller@barlowresearch.com.